SEC Qualified / REG A+ / CIK: 191904

A fixed-income corporate bond with daily compounding, backed by real estate bridge loans and U.S. Treasuries. Full liquidity. No lock-ins. No fees.

Bond overview

Why CREB

Compound Real Estate Bonds (CREB) is an SEC-qualified Reg A+ bond that pays a fixed 8.50% annual yield, compounded daily. Investor capital is deployed into short-term, secured real estate loans alongside a reserve of U.S. Treasuries. This overview sets out the principles that define the product and the rationale for the underlying asset class.

Annual yield

Compounding

Backing

Structure

Fees

Minimum

CREB is structured with a focus on preserving investor capital through short-term duration real estate loans, conservative underwriting standards, diversified exposure, and reserve allocations to U.S. Treasuries and cash.

review the offering

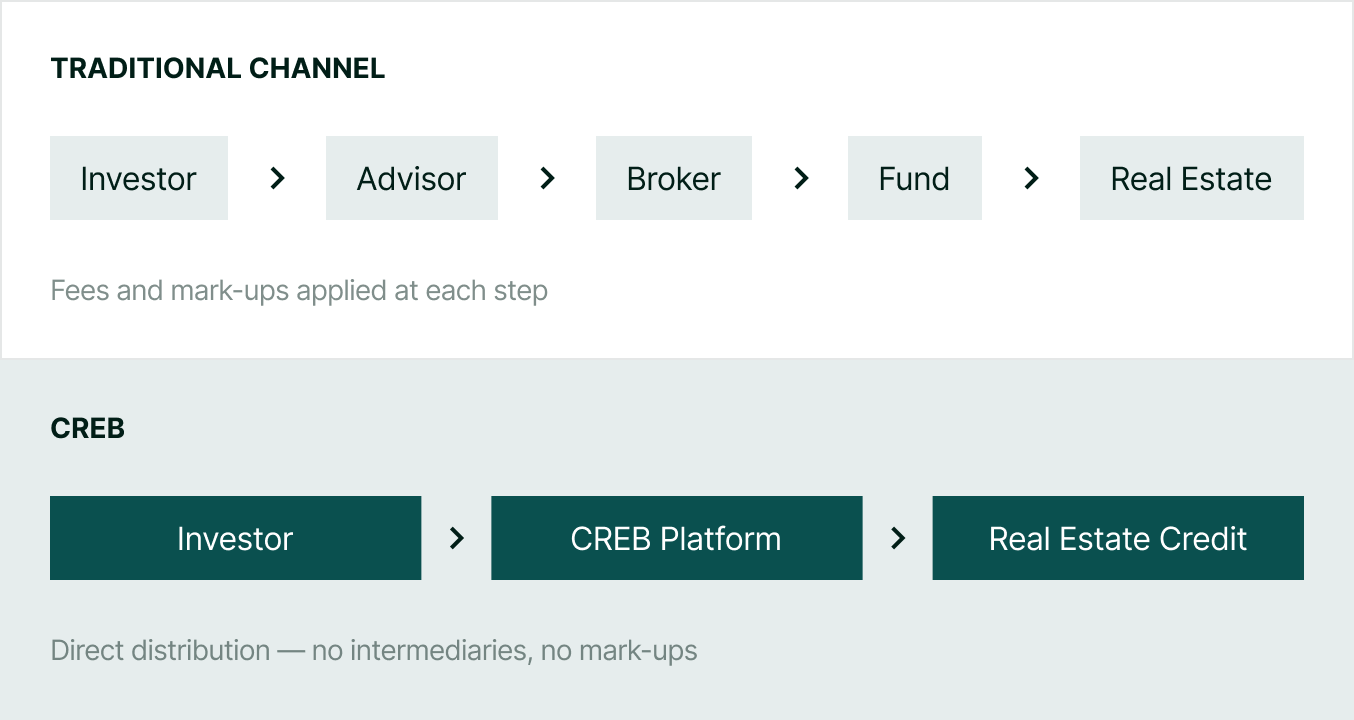

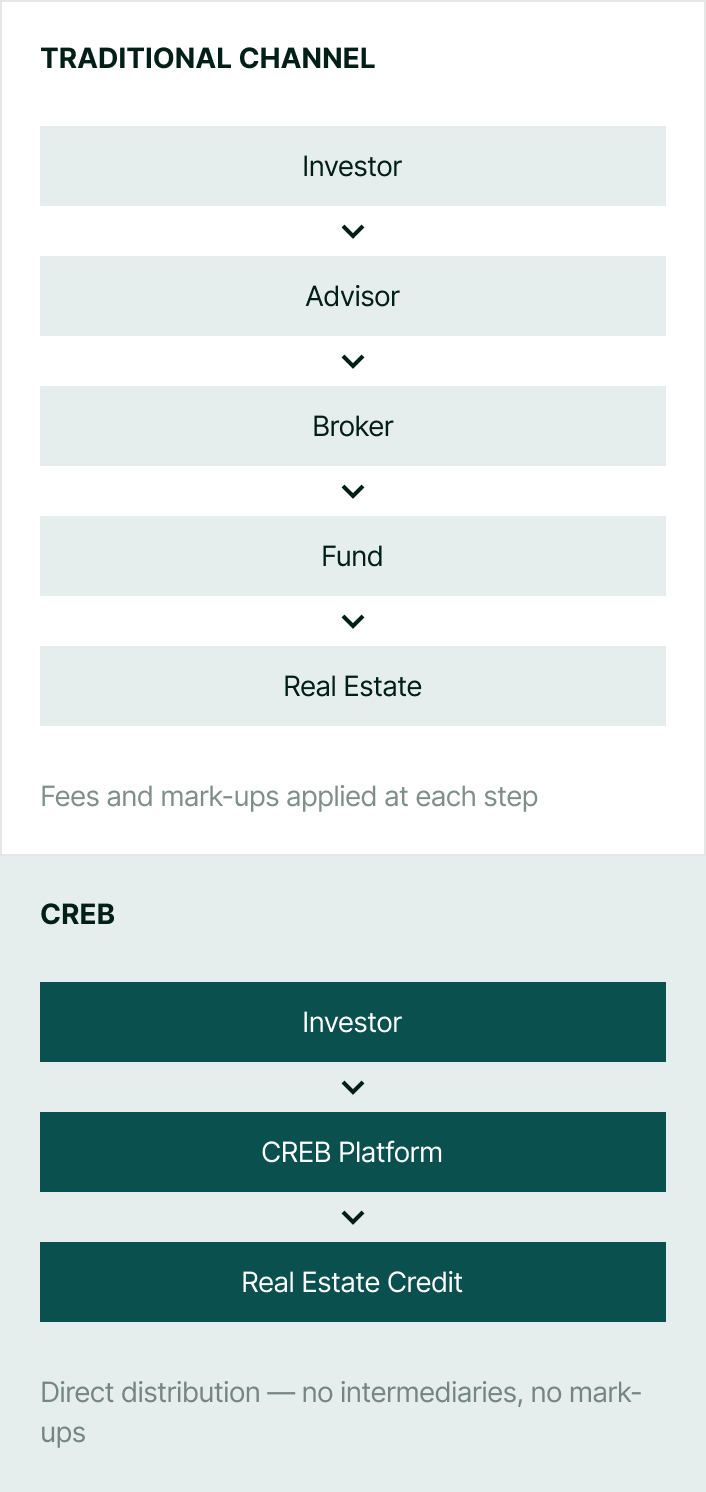

CREB is offered through a single digital platform, accessible by web and mobile. By distributing directly rather than through advisers, brokers, and intermediaries, the structure removes the layered fees and mark-ups associated with traditional channels.

Bond overview

Investor

Advisor

Broker

Fund

Real Estate

Fees and mark-ups applied at each step

CREB

Investor

CREB Platform

Real Estate Credit

Direct distribution — no intermediaries, no mark-ups

As an SEC-qualified Reg A+ Tier 2 offering, CREB files its financial statements publicly. Investors and their advisers can review the offering circular and audited financials in full before investing.

read the documents

CREB applies no management, account, or withdrawal fees, and imposes no lock-in period. Redemption requests may be submitted at any time, subject to standard processing.

The minimum investment is $500. The bond is available through both taxable (cash) and tax-advantaged (IRA) accounts, extending institutional-style real estate credit to a broad range of investors.

Asset class

Why Real Estate Credit

Real estate is the largest asset class globally. Lending against it — real estate credit — has historically generated income above traditional fixed income, secured by tangible collateral. CREB provides access to this asset class through a single regulated instrument.

The portfolio earns interest on short-term real estate loans — a return driven by lending activity rather than property-price appreciation. This supports a consistent, contractual income rather than variable, market-dependent gains.

CREB is structured with a focus on preserving investor capital through short-term duration real estate loans, conservative underwriting standards, diversified exposure, and reserve allocations to U.S. Treasuries and cash.

CREB lends rather than owns. Income is tied to interest payments secured by real property, keeping returns connected to tangible collateral rather than equity-market sentiment.

Returns from real estate credit have historically shown low correlation to public equities. Held alongside stocks and bonds, the asset class can reduce a portfolio’s overall reliance on public markets.

Next steps

Review the Offering

A full account of the loan process, portfolio holdings, and risk factors is available in the remaining sections of this overview.

This overview is a summary provided for informational purposes only and does not constitute an offer to sell or a solicitation to buy any security. Full terms, fees, and risk factors are set out in the offering circular, available under Documents. CREB is not a bank deposit and is not FDIC insured; investments are subject to risk, including the possible loss of principal. Yields shown are contractual and not a guarantee of future results.

Insights

Company News & Insights

Q1 2025

All scheduled investor payments were distributed on time and paid daily.

learn moreQ1 2025

Invest through Traditional, Roth, and SEP IRAs with tax advantage access to CREB.

learn moreInvest in diversified real estate lending designed to generate stable income, preserve capital, and provide flexible access to your funds.

FAQs

Frequently Asked Questions

Why are investors choosing CREB?

CREB was designed as a simple direct-to-investor platform focused on income, transparency, accessibility, and ease of use.

What makes CREB different?

Investors can manage their accounts digitally through the CREB dashboard, monitor earnings, track balances, and manage withdrawals directly online.

Why does CREB not use traditional middlemen?

CREB’s platform structure is designed to reduce unnecessary intermediary layers between

investors and the underlying investment strategy.

Why do investors consider alternatives to traditional savings products?

Many investors are seeking income-oriented alternatives due to declining savings yields, inflation concerns, and long-term income planning needs.

Why does CREB focus on income-producing assets?

Income-producing assets may provide contractual cash flow, real asset backing, and lower volatility characteristics relative to many traditional equity investments.

View Full Investor FAQs

Understand how CREB genrates income, manages liquidity, and seeks to protect capital.

how it works

Where Your 8.50% Comes From

How your money generates consistent returns

Number of holdings: 08

As of04/24/2026

step 1

You invest — capital enters an SEC-qualified offering

Choose Cash Account or IRA. Minimum $500. Verify identity via Plaid.

step 2

Capital invested across 5 asset classes

Bridge loans (55%), MBS (15%), RE funds (10%), Treasuries (10%), cash reserves (10%).

step 3

Portfolio earns 10–14%

Borrowers pay premium rates for speed. Banks take months — CREB funds in days.

step 4

The spread: 10–14% in, 8.50% out

You receive a fixed 8.50%. CREB retains 1.5–5.5% as revenue.

step 5

You earn 8.50% daily

Interest calculated on full balance every day including previously earned interest.

Get Started

How to Invest in Three Steps

Sign up online in minutes. Choose Cash or IRA. Verify identity via Plaid.

Link bank account, transfer from $10. Or rollover IRA/401(k). No fees.

Interest begins day one. Track in your dashboard. Withdraw anytime.

Daily Compounding

Product

Fixed-income corporate bond issued by Compound Real Estate Bonds, Inc. $10 face value

Interest Calculation

8.50% APY calculated daily on total balance. Formula: Balance × 0.085 ÷ 365

Liquidity

Withdraw anytime. Standard: 5–6 business days

Illustrative Income

As of 03/31/2026

Investment

monthly, USD

annual, USD

$10,000

$71

$850

$25,000

$177

$2,150

$50,000

$354

$4,250

$100,000

$708

$8,500

$250,000

$1,771

$21,250

Track Record

As of 03/31/2026

Total Bond Offerings

Active Investors

Principal Losses

Interest Paid On Time

Invest in diversified real estate lending designed to generate stable income, preserve capital, and provide flexible access to your funds.

Insights

Company News & Insights

Q1 2025

All scheduled investor payments were distributed on time and paid daily.

learn moreQ1 2025

Invest through Traditional, Roth, and SEP IRAs with tax advantage access to CREB.

learn moreFAQs

Frequently Asked Questions

How do I get started?

Investors can create an account online, complete identity verification, connect a bank account, and fund their account digitally through the CREB platform.

Are there fees?

No. CREB does not charge management fees, platform fees, or hidden investor account fees. Investors earn the stated net rate directly through the platform.

Is there a lock-up period?

No. CREB is designed to provide full liquidity and flexibility through the investor dashboard.

Can I withdraw my money at any time?

Yes. Investors may request withdrawals directly through the online platform subject to standard processing timelines.

How long do deposits take?

Funding timelines may vary depending on banking institutions, ACH settlement, and verification requirements.

When does interest begin accruing?

Interest generally begins accruing after deposited funds have settled and become fully invested.

Can I monitor my investment online?

Yes. Investors can monitor balances, earnings, transactions, and account activity directly through the CREB dashboard.

View Full Investor FAQs

Understand how CREB genrates income, manages liquidity, and seeks to protect capital.

Portfolio Allocation

Where Your Capital is Invested

Number of holdings: 08

Bridge loans lead for highest risk-adjusted returns.

Investment

Allocation

Real estate lending

55%

Mortgage-backed securities

15%

Institutional re funds

10%

U.S. Treasury bills

10%

Liquidity reserve

10%

Multi-family leads due to rental demand.

Investment

Allocation

Multi-Family

45%

Commercial

30%

Industrial

15%

Mixed-Use

10%

High-growth U.S. markets.

Investment

Allocation

South

35%

West

30%

Northeast

25%

Midwest

10%

*Portfolio allocations shown are illustrative and may vary based on market conditions, asset manager allocation decisions, liquidity management, and investment opportunities.

PORTFOLIO STRUCTURE

Core underwriting parameters for the underlying real estate credit portfolio.

Parameter

CREB Standard

Loan Type

First lien bridge loans

Typical Size

$500K – $5M

term

6 – 24 months

Interest Rate

10% – 14% (fixed)

Maximum LTV

75% (target 60–70%)

Property Types

Multi-family, commercial, industrial, mixed-use

Collateral

Real property, first-position lien

Exit Strategy

Refinance or property sale

PORTFOLIO STRUCTURE

Every bridge loan originates against defined criteria.

$2.1M

Loan Amount

65%

LTV Ratio

12.5%

Interest Rate

14 months

Term

First lien

Security

Multi-family

Property

*Anonymized example

Built Around Capital Preservation

CREB's portfolio is structured with multiple layers of risk manegement designed to support stable income generation, liquidity, and downside protection across changing market environments.

Senior Secured First-Lien Lending

All loans are secured by first-position liens on income-producing real estate.

Conservative Underwriting

We maintain conservative loan-to-value targets and strong borrowers targets.

Diversified Real Estate Exposure

Broad diversification by property type, borrower, and geography to reduce concentration risk.

Institutional Credit Allocation

Real estate credit is the core allocation, supported by high-quality reserves.

Treasury and Liquidity Reserves

A portion of the portfolio is allocated to U.S. Treasuries and cash equivalents for stability and liquidity.

Ongoing Monitoring and Stress Testing

Continuous portfolio monitoring, asset reviews, and stress testing to help manage risk proactively.

Insights

Company News & Insights

Q1 2025

All scheduled investor payments were distributed on time and paid daily.

learn moreQ1 2025

Invest through Traditional, Roth, and SEP IRAs with tax advantage access to CREB.

learn moreInvest in diversified real estate lending designed to generate stable income, preserve capital, and provide flexible access to your funds.

FAQs

Frequently Asked Questions

What is included in the CREB portfolio?

The CREB portfolio may include senior secured real estate credit, institutional real estate debt exposure, U.S. Treasury allocations, and liquidity reserves.

Why does CREB focus on real estate credit?

Real estate credit can provide income through contractual payment obligations while being supported by underlying real asset collateral.

What does senior secured mean?

Senior secured investments are generally positioned higher within the capital structure and are typically backed by collateral, which may help provide additional downside protection.

How does CREB manage portfolio risk?

CREB manages risk through underwriting discipline, diversification, collateral review, liquidity management, and ongoing portfolio monitoring.

Why does CREB hold Treasury and liquidity reserves?

Treasury and liquidity allocations are designed to support portfolio flexibility, risk management, and investor liquidity needs.

Does CREB invest in speculative development projects?

CREB’s strategy emphasizes income-oriented, asset-backed investment opportunities aligned with conservative underwriting and portfolio objectives.

How is the portfolio diversified?

CREB seeks diversification across investment types, borrowers, collateral, maturities, and liquidity layers to help reduce concentration risk.

What happens if market conditions change?

CREB’s portfolio approach is designed to remain disciplined across changing market environments, with a focus on income, collateral quality, liquidity, and capital preservation principles.

View Full Investor FAQs

Understand how CREB genrates income, manages liquidity, and seeks to protect capital.

Lending Standards

Key facts. Read the Offering Circular before investing.

Compound RE Bonds, Inc.

Issuer

Fixed-rate corporate bond

Security

8.50% APY

Coupon

Daily compounding

Interest

$10 / bond

Face Value

$10

Minimum

On demand

Maturity

$0

Fees

SEC Reg A+ Tier 2

Regulation

1919204

CIK

Up to $75M

Offering Size

U.S. residents, 18+

Eligibility

Corporate Structure

Entities and leadership managing your investment.

Parent

Compound Banc RE Holdings, Inc.

Issuer

Compound Real Estate Bonds, Inc.

Lending

Compound Lending, LLC

Founded

2021 (FL & DE)

Head Quarters

NY, United States

CIK

1919204

Materials

Documents & SEC Filings

Download latest security documents here

Document Name

Type

Description

Last updated

Bond Fact Sheet

CREB Investment Guide

SEC EDGAR Filings

All filings — CIK: 1919204

04/24/2026

download

Unsecured bonds: Not backed by specific pledged assets.

Not FDIC insured: Risk of loss including principal.

Early-stage company: Incorporated 2021. Limited history.

Real estate risk: Affected by economic conditions and rate changes.

Liquidity risk: Over $50K may take 30 days.

Concentration risk: Portfolio concentrated in RE assets.

Read the Offering Circular before investing.

Insights

Company News & Insights

Q1 2025

All scheduled investor payments were distributed on time and paid daily.

learn moreQ1 2025

Invest through Traditional, Roth, and SEP IRAs with tax advantage access to CREB.

learn moreInvest in diversified real estate lending designed to generate stable income, preserve capital, and provide flexible access to your funds.

FAQs

Frequently Asked Questions

Are CREB offerings regulated?

Yes. CREB offerings are conducted pursuant to U.S. securities regulations and qualified under Regulation A+ Tier 2 with the U.S. Securities and Exchange Commission.

Is CREB SEC qualified?

Yes. CREB offerings have been qualified by the U.S. Securities and Exchange Commission under Regulation A+ Tier 2. Qualification does not imply SEC approval or endorsement.

Where can I review offering documents?

Offering materials, disclosures, risk factors, and investor documents are available through the investor portal and offering pages.

Are financial statements available?

Yes. Applicable financial disclosures and filings are made available in accordance with offering and regulatory requirements.

Can I contact Investor Relations?

Yes. Investors may contact Investor Relations for assistance regarding offerings, onboarding, account questions, or general support.

View Full Investor FAQs

Understand how CREB genrates income, manages liquidity, and seeks to protect capital.