Last Updated:

June 20, 2026

6 min

.

read

When it comes to saving money, most people instinctively turn to traditional savings accounts. They’re safe, easy to use, and offer quick access to your cash. But there's one major downside — the interest rates are notoriously low. In fact, many savings accounts today offer rates so minimal that they barely outpace inflation, if at all.

This has led many savvy savers and investors to ask a simple question: Is there a better way to grow my money?

Enter real estate bonds — an increasingly popular investment option offering significantly higher returns without the complexity of managing a property. In this blog, we’ll break down what real estate bonds are, how they stack up against savings accounts, and why they might be a smart alternative for your financial future.

Understanding Savings Accounts

A savings account is one of the most common financial tools used by individuals to store money safely. Offered by banks and credit unions, these accounts are designed to help people put aside funds they don’t plan to use for daily expenses. Whether you're building an emergency fund, saving for a vacation, or setting money aside for future goals, a savings account is often the first step in a person’s financial journey.

How It Works

When you deposit money into a savings account, the bank pays you interest on your balance. This interest is typically compounded daily or monthly, allowing your savings to grow — albeit slowly — over time. The bank, in turn, uses your deposited funds to issue loans and earn profits, sharing a small portion of that return with you in the form of interest.

Pros of Savings Accounts

Easy Accessibility

Savings accounts are highly liquid, meaning you can access your money anytime through online banking, ATMs, or by visiting a branch. While there may be limits on the number of withdrawals per month, you can usually move funds to your checking account instantly if needed.

Safety and Security

One of the biggest advantages of a savings account is its safety. In the United States, the Federal Deposit Insurance Corporation (FDIC) insures bank deposits up to $250,000 per depositor, per bank. For credit unions, similar protection is provided by the National Credit Union Administration (NCUA). This means your money is protected even if the bank fails.

Simplicity

Savings accounts are straightforward. There are no complicated terms, fluctuating returns, or investment decisions to make. It’s a “set it and forget it” option — ideal for beginners or those looking for a hassle-free way to save.

Cons of Savings Accounts

Low Interest Rates

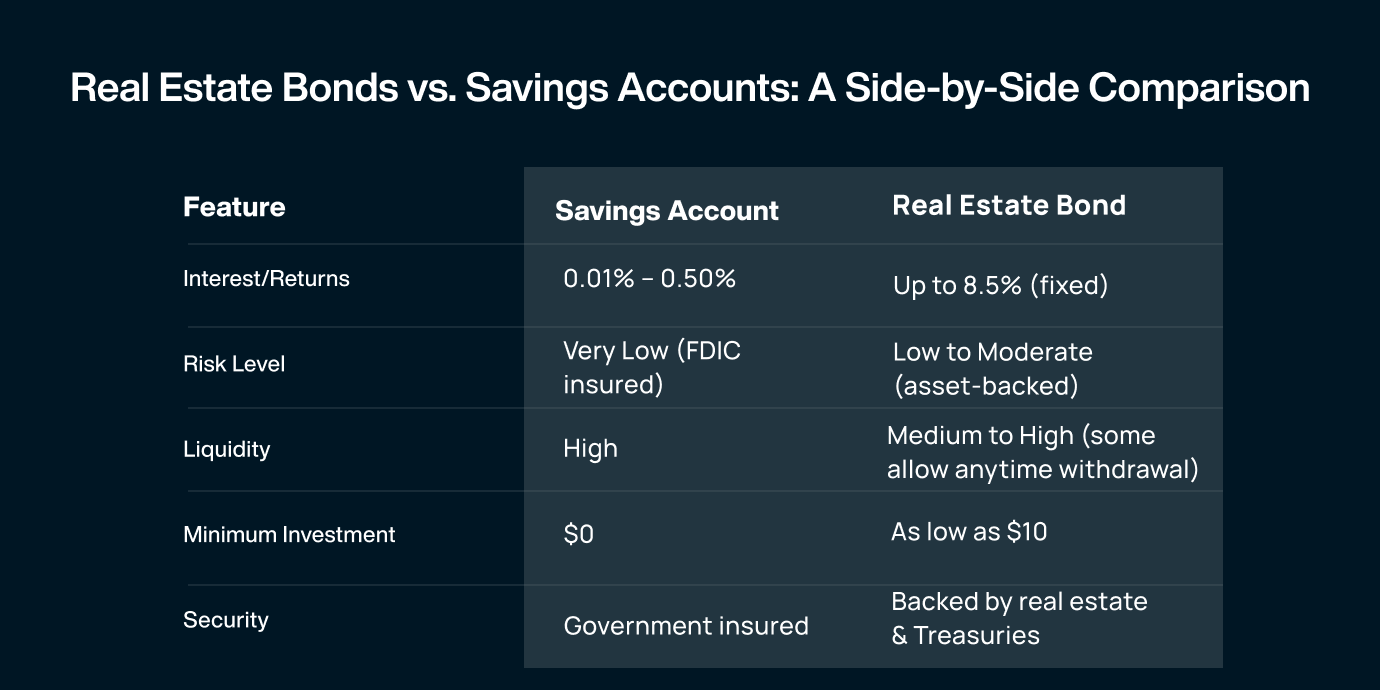

The biggest drawback is the extremely low return. Most traditional savings accounts offer annual percentage yields (APYs) between 0.01% and 0.50%. Even high-yield savings accounts often don’t break past 1.00%. This means your money grows very slowly — often not fast enough to outpace inflation.

Inflation Risk

Inflation reduces the purchasing power of your money over time. If your savings account earns 0.05% APY while inflation is 3%, you’re effectively losing money in real terms. While your balance might increase slightly, its value in terms of what it can buy is actually decreasing.

Opportunity Cost

By keeping your money in a low-yield savings account, you may be missing out on more profitable opportunities. Alternatives like real estate bonds, certificates of deposit (CDs), or low-risk investments can offer significantly higher returns, especially for long-term savers.

What Are Real Estate Bonds?

Real estate bonds are a type of fixed-income investment where you, as the investor, lend money to a real estate developer, company, or platform. In essence, they function much like traditional bonds — you’re not buying a piece of property, but rather providing the capital needed to finance real estate projects or loans. These could include residential developments, commercial buildings, or property-backed lending ventures.

In exchange for your investment, you receive a fixed interest payment, typically paid on a regular schedule — monthly, quarterly, or annually — over a set period of time. When that period ends (also called the bond’s maturity date), you receive your original investment (the principal) back.

How They Work

Let’s say a real estate company wants to renovate a commercial property or develop a new apartment complex. Instead of taking out a traditional bank loan, they might raise money by issuing real estate bonds. Investors like you can purchase these bonds, essentially acting as lenders. The company uses your money to fund the project, and in return, commits to paying you a pre-determined interest rate — often much higher than what you’d earn in a savings account.

Because these bonds are typically secured by physical real estate assets, your investment is backed by something tangible. This adds an extra layer of protection compared to unsecured debt or more volatile assets like stocks.

These bonds are often backed by tangible real estate assets — making them more secure than many unsecured investment options. For example, platforms like Compound Real Estate Bonds offer bonds that are backed by both real estate and U.S. Treasuries, providing added layers of protection.

Key Features:

- Fixed APY (Annual Percentage Yield): Often significantly higher than traditional accounts — Compound offers 8.5% APY.

- Low Entry Point: Start investing with as little as $10.

- Passive Income: Earn interest daily or monthly without lifting a finger.

Flexibility: Some platforms offer anytime withdrawals, making it more liquid than traditional bonds.

Benefits of Investing in Real Estate Bonds

- Higher Returns

Compared to the minimal interest earned in savings accounts, real estate bonds offer a substantial fixed return. At 8.5% APY, your money works significantly harder. - Passive Income Stream

You earn regular interest payments — daily, weekly, or monthly — providing a consistent cash flow. - Asset-Backed Security

Unlike stocks or crypto, your investment is tied to real assets like property or Treasury-backed loans. - Easy to Start and Manage

Platforms like Compound make it easy to set up an account, invest with just a few clicks, and automate your contributions. - Smart Saving Tools

With features like auto-investing and round-ups, your spare change and recurring contributions can grow quietly in the background.

Who Should Consider Real Estate Bonds?

Real estate bonds are not just for seasoned investors — they’re an accessible, practical option for a wide range of people looking to grow their money more effectively than a traditional savings account. If you're wondering whether this investment route suits you, here are some profiles of individuals who can truly benefit from adding real estate bonds to their financial strategy:

💰 Savers Looking for Better Returns

Do you have money sitting in a savings account, barely earning interest? Most traditional bank accounts offer returns so low they barely make a dent in your financial growth. Real estate bonds present a compelling alternative, often offering fixed annual returns significantly higher than those of savings accounts — in some cases, up to 8.5% or more annually.

These bonds allow you to put your idle cash to work, earning steady income without subjecting your money to high risk or complex investment strategies.

📆 Long-Term Planners

If you’re someone who’s thinking ahead — planning for retirement, a child’s education, or even future home ownership — real estate bonds are a smart fit. These investments typically span 1 to 5 years, making them ideal for medium- to long-term wealth-building goals.

You can invest with a “set it and let it grow” mindset, knowing that your capital is working in the background while you focus on your bigger life goals.

💸 Passive Income Seekers

Not everyone has the time or desire to actively trade stocks, follow market news, or manage rental properties. Real estate bonds offer a hands-off way to earn passive income, with predictable interest payments delivered on a regular basis — monthly, quarterly, or annually.

It’s a great solution for anyone who wants financial peace of mind and steady income without being tied to the volatility of the stock market.

📊 Diversification-Minded Investors

A well-balanced portfolio is essential for managing risk and achieving consistent returns. If your investments are heavily concentrated in one asset class — like stocks or mutual funds — adding real estate bonds can provide much-needed diversification.

Because they’re often secured by real assets, real estate bonds tend to be more stable and less correlated with market swings, offering protection during periods of volatility.

Real-Life Example: Compound Real Estate Bonds

One platform making real estate bonds accessible to everyday investors is Compound Real Estate Bonds. Here’s what sets them apart:

- 8.5% APY — a strong fixed return in today’s low-rate environment

- No fees — what you earn is what you keep

- Anytime withdrawals — get your money when you need it

- Low entry point — start with as little as $10

- Auto-invest & Round-ups — grow your money effortlessly

- Backed by real estate and U.S. Treasuries — a unique blend of security and performance

It’s a smart, secure, and modern way to grow your savings faster than traditional accounts.

Conclusion

Traditional savings accounts are safe — but they rarely grow your wealth. If you’re looking to earn more from your idle cash without diving deep into volatile markets, real estate bonds offer a compelling alternative.

With higher fixed returns, real asset backing, and tools that make investing easier than ever, real estate bonds can help you make smarter financial decisions — and reach your goals faster.

Ready to make your money work harder?

Explore how Compound Real Estate Bonds can help you earn 8.5% APY with no fees, anytime withdrawals, and smart investing tools built for you.

share the article